WEALTH MANAGEMENT INSIGHTS

Winning Women’s Wealth

Why “More Women” Isn’t a Strategy

9 min read

Author

Katia Sand

Talk to leaders from the U.K.’s top financial services firms and several will tell you that a key element of their 2026 strategy is to become a top destination for female wealth.

That ambition is timely, as the segment is expanding faster than the broader market. And while women control a rising share of investable assets, they remain underserved by the current financial model. It’s not surprising that wealth managers among SBR’s clients across the U.K. and the U.S. see engagement with female clients not just as an opportunity, but as a competitive necessity.

However, the firms that go beyond lip service to actually win market share aren’t just going to define “women” as their target customer. If they want to make a real difference, they’ll have to go deeper into precise ideal client profiles (ICPs) and build segment-specific go-to-market (GTM) strategies. Success will depend on tailored messaging, clearly articulated value, and services that help women feel their specific personal load has been heard, understood, and lightened.

The urgency: women’s share of wealth is rising fast

Recent trends show the scale of the opportunity. From 2018-2023, global wealth grew 43%, but wealth controlled by women grew 51%. In the U.S. and Europe, women currently control about one third of retail financial assets, a share expected to rise to 40–45% by 2030. In the U.S. specifically, women are on track to control $34 trillion in investable assets by 2030.

Women are expected to control 40-45% of retail assets in the U.S. and Europe by 2030.

These numbers highlight a clear turning point: women’s influence over wealth is stronger than ever. This trend reflects not just generational transfers, but also the rise of divorcees, female entrepreneurs, and women advancing across diverse careers. Collectively, they are reshaping the financial landscape, and firms that ignore this shift risk missing the commercial opportunity and falling behind.

The complication: disparity is still the reality

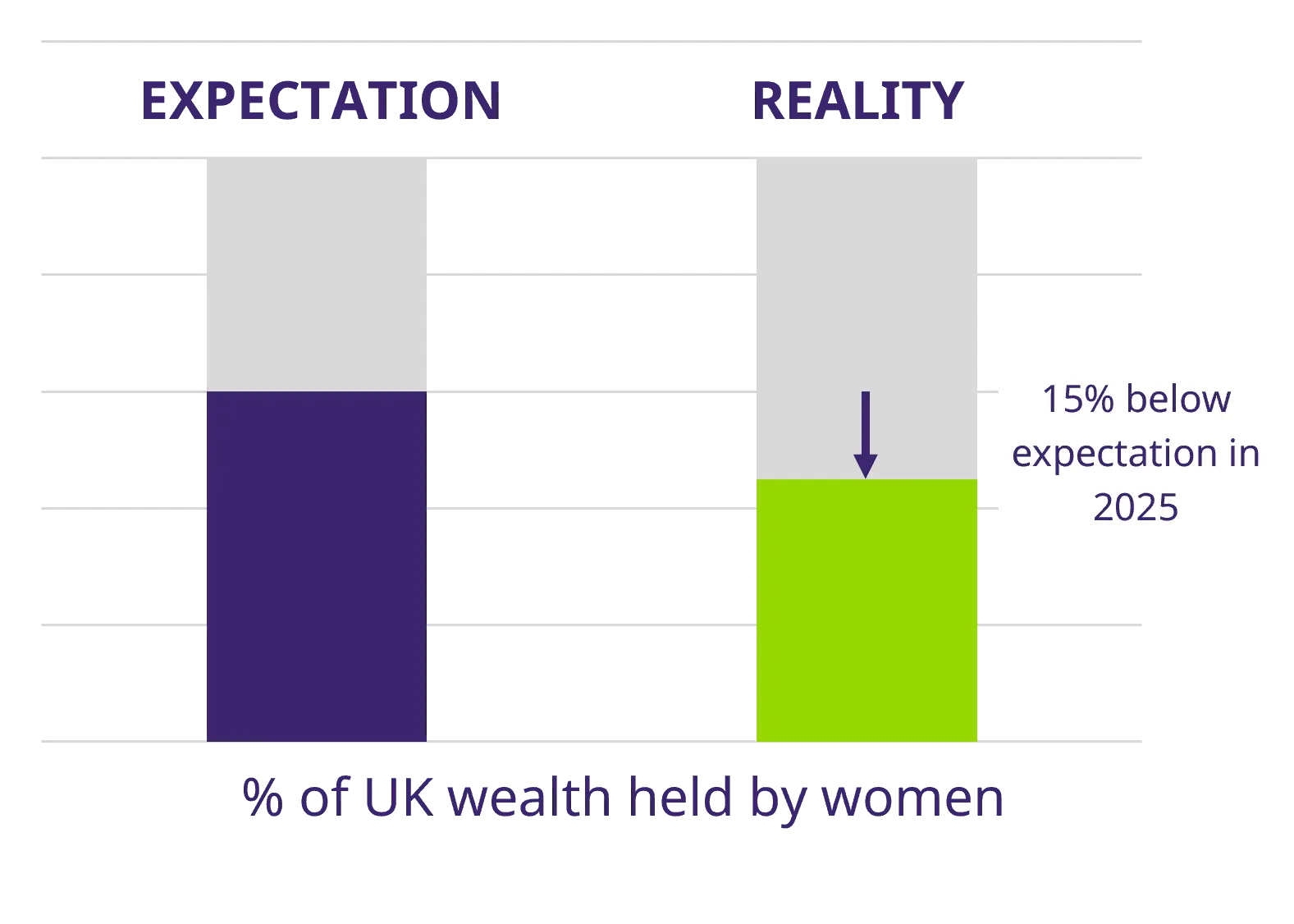

While we’re at a turning point, the world hasn’t changed overnight. The Centre for Economics and Business Research projected that women would hold 60% of U.K. wealth by the end of 2025. But as women across the country juggle rising household costs and silently scream at forecasters, “Show me the money!”, it’s become clear that those projections didn’t quite play out as expected. The latest ONS analysis shows that women actually hold closer to 45% of personal wealth.

A big part of that gap comes down to pensions. Official data show U.K. women’s private pension wealth is substantially lower than men’s across most age groups. Similarly, broader studies estimate that women in the U.S. are likely going to retire with roughly three-quarters of men’s wealth, on average. This doesn’t just reflect differences in pay and career trajectories, but also investment participation and accumulation. Other studies show that more than half of women’s wealth is tied up in property and physical assets, often shared with partners.

The result is a persistent overall 21% gender wealth gap in the U.K. and roughly a 30% gap in the U.S. Despite controlling more wealth, women still aren’t as active in financial markets as their male counterparts. In practice, this means that while women are acquiring and accumulating assets, they are still less likely to translate that wealth into long-term growth. The need for sound, relevant advice is real.

Women were expected to hold 60% of U.K. wealth by 2025, but the latest analysis shows that number is closer to 45%.

The compounding effect: women engage less with wealth managers

So women’s wealth is growing but hasn’t yet caught up to men’s, largely because women participate less in financial markets. This gap won’t close by itself, and you might expect it to drive more women to seek advice. Yet they also remain less likely than men to engage with wealth managers, leaving a significant pool of unmanaged assets. More than half of women in the U.K. and U.S. report never having invested. Many are more cautious about risk, and a majority want greater confidence in retirement planning. A global study by BNY Mellon shows that if women invested at the same rate as men, $3.22 trillion of additional capital would enter the market, yet only 28% of women feel confident investing today.

Managing money is a centuries-old tradition for men. It’s only been several decades for women.

But why are women less likely to seek investing help? In a recent conversation, friends and I asked what about our upbringing, education, or perhaps even nature made us less inclined to ask for advice. One major factor quickly became clear: most traditional financial services models simply don’t cater to women.

Analyses have previously pointed to common patterns among women: greater risk aversion, a preference for stability, and a focus on savings and family security. These analyses weren’t wrong per se, but their findings have been flattened into a single narrative, encouraging firms to treat women as one uniform segment. Assumptions around longevity, retirement planning, and career interruptions are applied wholesale, masking significant differences in financial goals, confidence, and intent.

This highlights a clear opportunity: firms that tailor their services to individual women’s priorities and preferences, build confidence, provide clarity, and address life-stage complexities, can help these clients engage more actively and effectively in building wealth.

Related: The Growth Workshop Podcast: Purpose, Leadership and Inclusive Wealth with Rachael Smith of Evelyn Partners.

If women invested at the same rate as men, $3.22 trillion of additional capital would enter the market.

Targeting women with precision: defining ideal client profiles and go-to-market strategies

Knowing all this, the lesson for financial services leaders is clear: “more women” is not a strategy. Successfully navigating the gender shift in wealth means moving beyond broad assumptions and focusing on granular micro-segments with tailored engagement models for each. In other words, serving real women with concrete financial needs, instead of treating women as a single group defined by lower risk tolerance or an excessive preference for security, both of which can limit long-term wealth creation.

At SBR Consulting, we help organisations clearly define their most relevant ICPs and translate those insights into segment-specific go-to-market strategies. By clarifying who their clients are, how best to reach them, and how to track outcomes, firms can move from market understanding to measurable impact.

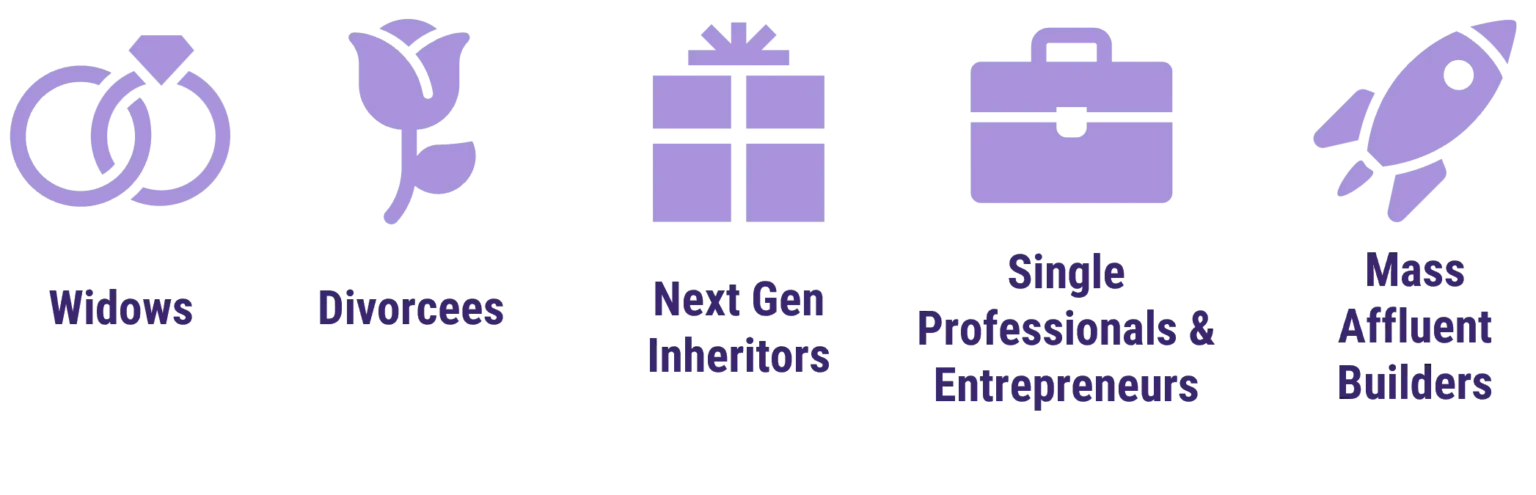

Well-defined ICPs: meeting women where they are

Knowing all this, the lesson for financial services leaders is clear: “more women” is not a strategy. Successfully navigating the gender shift in wealth means moving beyond broad assumptions and focusing on granular micro-segments with tailored engagement models for each. In other words, serving real women with concrete financial needs, instead of treating women as a single group defined by lower risk tolerance or an excessive preference for security, both of which can limit long-term wealth creation.

1. Widows

Women disproportionately outlive men and often manage assets later in life. Sudden wealth transfers (inheritances, retirement accounts, and insurance proceeds) are common.

How firms could serve them: Widows are often overwhelmed by financial complexity and feel underserved by firms that haven’t treated them as equal partners along the journey. Up to 80% switch advisors within a year of inheriting. Addressing “Mrs.” with the same care and respect as “Mr.” throughout the entire relationship can help retain assets not just during this period but also when the next generation eventually inherits.

2. Divorcees

Divorce can trigger a major shift in financial status, and women are frequently underprepared for managing their new financial reality while also navigating the emotional and practical upheaval of separation. This life change is typically experienced at a younger age and with different priorities than bereavement, making financial planning needs and risk tolerance distinct.

How firms could serve them: Divorce can push women into financial independence when they’ve had less time to prepare for the implications. Research shows that 65% of midlife women worry about their finances during divorce, yet 9 in 10 don’t seek advice. Tailored guidance here positions firms as trusted advisors at a critical junction, helping women feel confident, informed and supported. It’s hard to leave an advisor who has expertly helped you navigate an unexpected crisis.

3. Next-gen wealth heirs and beneficiaries

Next-gen wealth heirs and beneficiaries: Millennial and Gen Z women are increasingly stepping into financial decision-making roles as heirs and beneficiaries of family wealth. They tend to be digitally fluent, values-driven, and less trusting of traditional institutions, with a strong interest in socially responsible investing.

How firms could serve them: Many women in this segment inherit a parent’s advisory arrangement but expect a completely different mode of engagement. Firms that adapt early, multi-thread across generations, and provide values-aligned experiences can help these clients feel respected and empowered, building new, meaningful relationships rather than assuming legacy titles will suffice.

Related: The Growth Workshop Podcast: Financial Planning for a New Generation with Rebecca Williams of Rathbones.

4. Single professionals and entrepreneurs

A growing number of women are building wealth independently, either by prioritising career advancement or launching their own businesses. These women may have more complex financial profiles, and, without traditional household financial structures, they are typically the sole decision-makers and highly engaged in defining their financial goals.

How firms could serve them: Women in this segment often value advisory partnerships that are flexible, digitally enabled, and focused on building financial confidence without assumptions about family or lifestyle choices. Advisors who demonstrate a nuanced understanding of their risk tolerance, equity planning needs, tax optimisation, and long-term wealth structuring can position themselves as trusted strategic partners, helping these clients navigate complexity while supporting their personal and professional ambitions.

5. Mass affluent builders

Many mass affluent women hold meaningful savings alongside a steadily growing income but remain underinvested in long-term growth assets. They are often financially disciplined and security-focused, balancing competing priorities such as home ownership, childcare, elder care, and retirement planning. Despite financially responsible habits, hesitation around investment risk and complexity can slow wealth accumulation.

How firms could serve them: This group responds well to low-barrier entry points into investing, supported by clear and transparent guidance. Advisors who help translate cash savings into structured plans can build trust while demonstrating measurable progress. By simplifying decision-making and reinforcing confidence early, firms can establish durable partnerships as these clients shift assets and continue growing wealth.

The lesson for financial services leaders is that “more women” is not a strategy but micro-segments are.

Segment specific GTM: what winning looks like

Defining ICPs is just the start. The challenge, and the opportunity, is translating those insights into engagement that actually moves the needle. Too many wealth managers know the theory but treat every woman the same. The ones who’ll win are those who focus on the details that matter most for each micro-segment:

- Demographics: age, location, life stage

- Financial complexity: assets, equity compensation, business interests

- Unique values: ESG priorities, philanthropy

- Preferred ways to interact: in person, digital, or a mix

Tailor your proposition to each segment. Women don’t necessarily need a new product, but many need a different experience.

Once you’ve clarified these elements, everything else starts to fall into place. Messaging, advice, events, and digital experiences should all reflect what truly matters to each group. Then, outcomes tied to each GTM should be tracked closely, not just at a high level, but by ICP, so you can validate whether your definitions are right and your message is landing, resonating, and making a difference.

Some of these metrics may be familiar, but the real insight comes from connecting them to specific ICPs:

- Engagement: advice uptake, event attendance, digital learning completions

- Activation: cash to investment conversion, new account openings, first year contribution rates

- Retention and growth: net-new assets post inheritance, household share of wallet

- Experience and trust: NPS by segment, advisor match quality

Tracking these metrics by micro-segment gives advisors and firms a clear line of sight into whether their GTM strategies are actually delivering impact and where course-corrections are necessary.

Advisor representation matters

Not to be overlooked, having female representation at your firm matters. Men still wonder if having an all-female team is “too much,” but may not notice when the team may as well be a men’s sports locker room: a reality that women have had to navigate for years. U.S. advisor demographics are improving but still fall short of parity: women make up roughly 24% of advisors, while the figure is just 18% in the U.K.

Firms should set measurable goals for recruitment, mentorship, and leadership pathways, while also exploring ways to spark interest and develop skills in younger demographics – taking a leaf out of the STEM playbook.

Related: The Growth Workshop Podcast: Imagining Wealth Through Inclusive Leadership, with Rebecca Williams of Rathbones.

The resolution: purpose, precision, and proof

The firms that will become the “number one destination for female wealth” in the U.K. or U.S. won’t rely on broad slogans or generically diverse imagery. They’ll define granular ICPs and design ICP-specific go-to-market plays that meet women where they are, by life event, profession, risk comfort, and values.

At SBR Consulting, we specialise in helping financial services organisations move from where they are to where they want to be. We clarify value propositions and align training and performance metrics to enable advisors to translate insights into actionable strategies with the goal of executing measurable business impact. Contact us for a free consultation on how we can help your firm.

The firms that will win in the space are the ones who’ll tailor the right messaging to each segment and avoid generic “female-friendly” or pink-washed campaigns.